Adobe's 38% Collapse: CEO Exits an Overgrown Empire as AI Eats Its Lunch

Date: March 12, 2026

Ticker: ADBE

Author: EverHint Editorial

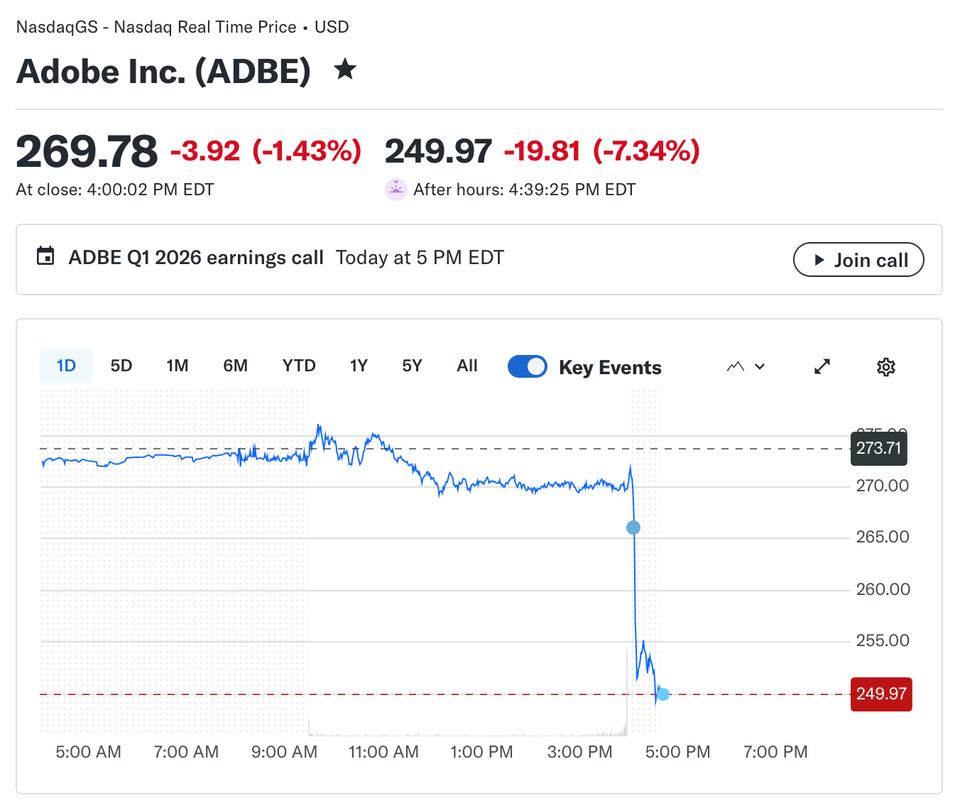

Adobe just delivered record Q1 results — $6.40 billion in revenue, $4.60 EPS — and the market's response was brutal. After-hours trading sent shares plunging to $252, adding to a staggering 38% decline over the past year. And now, CEO Shantanu Narayen, who led Adobe for 18 years, has announced he's stepping down.

The timing is not a coincidence.

The Numbers Don't Lie

A year ago, Adobe traded near $423. Today it closed at $269.78 — and is heading lower after hours. The 52-week range tells the whole story: $244.28 to $422.95. That's not a dip. That's a controlled demolition.

Even the record quarter couldn't stop the bleeding:

- Revenue: $6.40B (record)

- Net Income: $1.89B

- EPS: $4.60

- Revenue Growth: +3.3% QoQ

Wall Street expected more. The market wanted a reason to believe AI would save Adobe, not cannibalize it. Instead, it got a CEO departure and a guidance that failed to inspire confidence.

An Overgrown Monster

Adobe has become the textbook case of corporate bloat in Big Tech. With a $110 billion market cap and over 30,000 employees across a sprawling product empire — Creative Cloud, Document Cloud, Experience Cloud, Firefly, Express, Acrobat, and dozens of overlapping tools — Adobe is a bureaucratic machine that moves at the speed of a Fortune 500 committee.

The problem isn't revenue. Adobe prints money. The problem is that Adobe has become so large, so layered with middle management and redundant product lines, that it can't pivot fast enough when the ground shifts beneath it. And AI has shifted the ground violently.

Canva ships AI features in weeks. Midjourney disrupts image generation overnight. Open-source tools like Stable Diffusion threaten entire Adobe product categories for free. Meanwhile, Adobe's answer — Firefly — is impressive on paper but locked behind the same subscription walls that increasingly feel like a tax on creativity.

Layoffs Are Coming

Let's call it what it is: Adobe is ripe for a massive restructuring. When a CEO of 18 years announces his departure right alongside record earnings, the message is clear — the board wants a new direction, and new direction in Big Tech always means one thing: layoffs.

Adobe already cut 100 jobs in late 2024 focused on its sales organization. But that was a papercut compared to what's likely coming. The company's headcount has ballooned over the past decade through acquisitions (Figma deal collapsed, Marketo absorbed, Frame.io integrated) and organic hiring sprees that added layers of complexity without proportional revenue growth.

The math is simple. Adobe's revenue grew ~10% last year. Its headcount grew faster. Its stock dropped 38%. Something has to give, and it won't be executive compensation.

Expect the new CEO — whoever emerges from the search — to arrive with a mandate to cut deep. Thousands of jobs across Experience Cloud, redundant AI teams, and bloated enterprise sales could be on the chopping block. This is the playbook we've seen at Meta, Google, and Microsoft. Adobe's turn is overdue.

AI: Existential Threat or Overhyped Fear?

The bulls argue Adobe is monetizing AI disruption — Firefly-powered ARR tripled year over year, and subscription revenue grew 13%. Seeking Alpha analysts point to 41% FCF margins, a forward P/FCF of just 10x, and call the SaaS selloff "overdone."

They might be right on valuation. At a P/E of 15.78, Adobe is cheaper than it's been in a decade.

But cheap can get cheaper. The "AI disruption trade" that Benzinga flagged — the idea that generative AI makes Adobe's core creative tools less essential — hasn't played out in the financials yet. But it's playing out in the stock price, which means institutional investors are pricing in a future where Adobe's moat narrows. When Michael Burry buys your stock, it's either a genius contrarian call or confirmation that you're a deep value trap.

The CEO Transition Wildcard

Narayen will stay as Board Chair while the search for a successor plays out. Frank Calderoni, Lead Independent Director, is overseeing the transition. The question is whether Adobe taps an insider who preserves the status quo or brings in a turnaround operator.

If history is any guide, the board will choose disruption. They have to. Adobe's stock is down 57% from its all-time highs. Analysts still have a $378 consensus target — a 40% upside that feels more like wishful thinking than grounded analysis when the stock can't hold $270.

What Comes Next

Adobe isn't going bankrupt. It isn't even struggling, by traditional metrics. But the market is telling a clear story:

- AI competition is real and accelerating

- Corporate bloat has made Adobe slow to respond

- The CEO exit signals the board knows it

- Layoffs and restructuring are the logical next step

For investors, the 38% decline might eventually look like a buying opportunity — but not until the restructuring actually happens, the new CEO is named, and there's evidence Adobe can compete in an AI-first world without relying on subscription lock-in.

For employees, it's time to update the resume. When the CEO leaves and the stock is down 38%, the layoff emails aren't far behind.

This article reflects the editorial opinion of EverHint and is not investment advice. Always conduct your own research before making investment decisions.